Pros and Cons of Peer-to-Peer Lending for a Small Business

RELATED SOLUTIONS

Let’s stay in touch.Subscribe to our newsletter here.

The world of investing and borrowing hasn’t been immune to change. And peer-to-peer lending is one of the fastest growing trends in the world of finances right now. As more and more people start to question the reliability of traditional banks, many of them turn to alternative ways to make money. And whereas before the rise of FinTech, p2p was only possible within a rather small community, with the modern lending platforms the concept can finally scale.

So what peer-to-peer lending actually is in today’s technological environment? Put real simple, peer-to-peer lending is a kind of system that matches the investors who have specified the terms they are open to giving money away for and the borrowers who are evaluated and offered a choice of lenders based on their profile. Arguably the main reason why the whole idea is so catchy because it eliminates a lot of intermediaries who used to stand between borrowers and investors. And now they connect directly.

Investor logs into a system, sees the loan requests with evaluated risks and estimated returns, and decides, who they want to fund and at which terms. And since p2p isn’t as heavily regulated yet, the conventional risk evaluation rules don’t always apply. And even though, loan processing and origination is still an extremely important part of the process, the borrowers don’t need to convince a huge corporation that they deserve a loan. Instead, they need to present the data in an online application, let the automatic system evaluate them and let the investors directly decide whether or not they are eligible.

Overall, peer-to-peer lending, given that you choose the right platform, poses a unique opportunity both for investors and for borrowers to find exactly what they are looking for while the business owner takes care of most of the documents and ensures the security of the transactions.

But the kicker is that both investors and borrowers can get better conditions due to digitalization.

Is P2P lending regulated and if so, how?

Up until recently, P2P functioned pretty much as the new Wild West. And while it may be tempting to try and get money at a better interest rate and faster, you still need to make sure that the company is legit, that the investors are carefully selected and the whole venture is secure. That’s when regulators come into play.

It took them some time, but they adapted and aren’t idly accepting the malfeasance and scams of the industry which used to be very common. Of course, the specific regulations depend on the governing bodies in each specific jurisdiction, but overall the trend looks up. In most countries that allow proper online peer-to-peer lending, the following regulatory best practices are starting to take place:

- Platforms should take care of AML and KYC compliance, checking their end-users.

- The platforms are required to hold a capital reserve to mitigate financial risks for the lenders.

- Investors should have legal grounds to escalate unsuccessful loans cases.

- Platforms should provide investors with the truthful information about the return rates, expected dept rates, and the form of security platform has.

- Clear criteria of eligibility and risk evaluation of borrowers.

As more money pours into the p2p lending niche, authorities will make more efforts to control that field. And in my opinion, that’s a good thing. Look at how fast ICOs got discredited due to all the scams and cons in the industry. We wouldn’t want the same thing to happen to the great concept of peer-to-peer financing. And since the regulators already have some experience working with the digital-native financial institutions, we have all the reasons to hope that the regulation won’t be too oppressive.

Is peer-to-peer lending a good choice for small business?

So we’ve established that peer-to-peer lending is a big deal, but let’s go over the biggest advantages borrowers get when they choose this funding model for their needs.

Pros of peer-to-peer lending for borrowers

An easy and fast application process

Modern peer-to-peer lending only makes sense if the whole process if done fully online. This makes up for a huge competitive advantage of this model compared to working with traditional banks. Of course, that’s not just characteristic of p2p platforms, but rather most of the digital lending operations. Nonetheless. The loan origination and processing which used to take days and weeks, now, thanks to advanced automation solutions, can be condensed to 9 minutes of borrowers time.

At the same time, this fully depends on the platform lending company is using to automate their processes and on the origination engine, this platform has. The prime example of such a solution would be TurnKey Lender’s peer-to-peer automation platform which takes care of the company’s entire lending process both for investors and the borrowers. TurnKey Lender is the recognized technological leader in this domain with AI-driven intelligent proprietary risk evaluation and loan decisioning algorithms which are customizable and come built-in with the software.

Lower origination fee

Origination used to be one of the most time-consuming and costly parts of getting a loan. Depending on the company you worked with, it could cost you anywhere from 0.5% to 5% of your loan. But if you choose the right peer-to-peer lender who in term has chosen the right loan origination software, this process is automated and may even be powered by AI, so for the lender, the process involves less analysis and therefore the expenses are lower.

And it’s not just about origination. The extent of automation that the modern peer-to-peer platforms can have now lets them automate pretty much all the steps of the lending process which all required much more human labor before.

Chance for a better interest

Automation allows for many beautiful things. But probably the one that tips the scales for a run-of-the-mill borrower most would be the chance to get a better interest rate than with the traditional banks. Peer-to-peer lenders aren’t as heavily regulated and they don’t need immense staffs and wide-spread nets of branches around the country. All that, and not to mention, the reducing risks that come with AI-powered origination, is reflected in the interest rates you’d need to pay.

Faster Approvals

Old-school banks that still run on human processing or on legacy software don’t come even close to the speed and ease of application with a modern peer-to-peer platform. For a small or medium-sized business that needs money quickly for an expansion or to support everyday operation that might just be the ultimate advantage.

Initial quote that won’t affect the credit score

With most peer-to-peer platforms, the initial quote you get from the company won’t in any way reflect your credit score. This means that the company would only do a basic search of your data in the databases letting you scout for the best possible offer on the market without the unnecessary damage to your score in future applications.

Cons of peer-to-peer lending for borrowers

But as you’ve probably guessed peer-to-peer lending is no dreamland. These are real companies that need to make a profit at the end of the fiscal year and they operate accordingly.

Interest may be high

Yeah, you’re right, this one was in the pros part as well. It all depends on your credit score or on the other factors taken into account during risk evaluation by the company. With peer-to-peer lending, you are more likely to get a loan than with a traditional bank, but if your application isn’t that impressive be prepared to see that reflected in the terms you are offered.

Interest rates for borrowers with very low evaluation may go as high as whooping 36%. So just as with the traditional banks, you would want to take the repercussions to improve your credit score before you decide to apply.

Just as much responsibility

Failure to pay off a loan within a peer-to-peer platform will hurt your credit score and future eligibility just as hard as it would in any other case, so the borrower still faces just as much responsibility getting money this way.

Common application fee

The peer-to-peer economy isn’t completely middlemen-free. Someone does need to take care of the platform where borrowers and lenders cooperate. And it will either be reflected in the interest rates or, more commonly, there will be an application fee or a built-in quote within your loan to work with the platform.

Smaller loans

If you want to get a long-term home mortgage, p2p might not be the way to go. Generally, peer-to-peer companies are platforms where small to mid-size loans are getting quickly disbursed at larger volumes.

How to choose the P2P lending platform to fund your business

Credibility

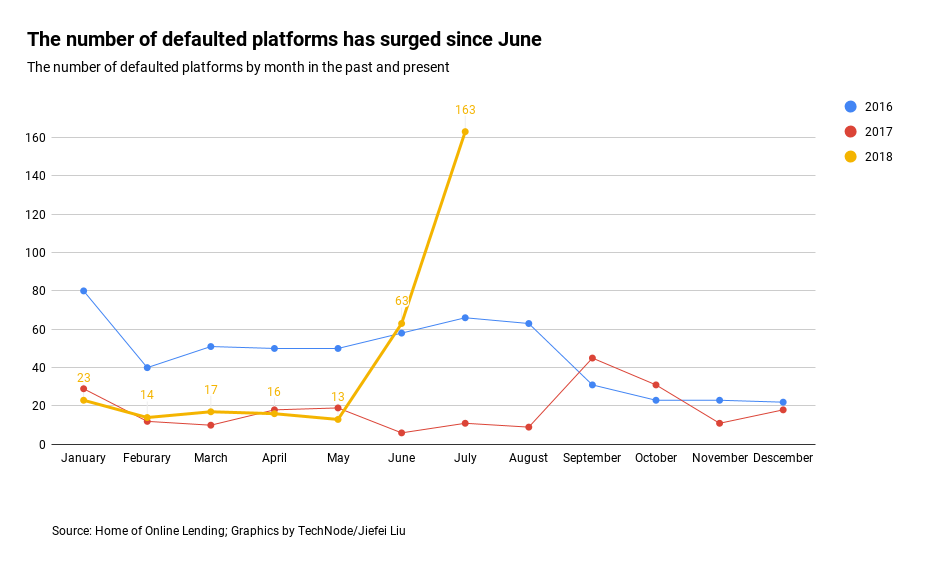

Unfortunately, P2P lending, like any other niche that works with money, has its fair share of fraud and scams. For example, in China, peer-to-peer lending saw a groundbreaking growth but once regulators started to zero-in on all the scams and semi-legal activities going on in the niche, the number of defaulted platforms skyrocketed. So both borrowers and investors should do thorough checks before committing to a company.

Are there any fees other than interest

The companies worth doing business with will be open about the monetization model they use. Be it a part of the interest rate that they keep to themselves, a flat application fee, or an origination fee – find out beforehand if the conditions suit you.

Ease of communication

No matter the loan size you’re seeking, you should be able to get in touch with a support representative of the company with any questions you have at any stage of the process.

Terms and eligibility criteria

Even before you register, you should be able to know all the information you may need. This can include the terms at which your loan will be distributed, how fast you should expect the money to arrive on your account or the criteria you’d need to meet in order to qualify for the loan at acceptable terms. Not to mention, the exact decisioning process your file will go through and the way the company will control you.

Final thoughts

Given the research and the right choice of the peer-to-peer lending company, this model may be a great opportunity for a business to get the funds it needs to work on new projects or to finance existing ones. And even though this field is still a newcomer in the world of financial products and services, the trend is likely to continue to go up. Which means that more borrowers and lenders will be joining in and reaping the benefits of using this funding model. And TurnKey Lender with its intelligent and easy-to-use lending automation solutions will be there to make the process for the peer-to-peer lenders, investors, and borrowers a bliss.

TurnKey Lender Editorial Team

Founded in 2014 and headquartered in Austin, TX, TurnKey Lender provides a cloud-based, AI-powered lending automation platform that enables lenders to digitize the entire loan lifecycle. The solution delivers decisioning, origination, servicing, collections, and compliance in one unified system, helping banks, credit unions, FinTechs, and embedded lenders scale efficiently while staying compliant. TurnKey Lender serves a global customer base. Visit www.turnkey-lender.com to learn more.